City Council meet on April 20th for its regular meeting with a light agenda. One item worth discussion is the Ordinance that setup the new Urban Redevelopment and Tax Increment Equivalent Fund (TIF) for the former Tri-County Mall.

The idea of the TIF can be daunting – don’t let the technical language be a instant turn off! Once you get past the name and look at what this Ordinance enables for the developer and the City at large it really is an exciting update.

(Additional disclaimer: I am not an attorney and this is by no means an exhaustive review of TIFs or even this particular TIF. TIF rules vary by State, and even in Ohio there are multiple sections of State Law that describes what is possible with TIF funds. This post is highlighting, summarizing, and sharing my thoughts on this with the current publicly available information. If you have specific questions or clarification asks just let me know and I can chase those down.)

TIF Overview

When an Urban Re-development Zone and TIF is setup the developer pays into this fund in place of typical property taxes – an important part here is that the value of the new improvements are exempt from property taxes during the life of the TIF, these payments are made in place of the property taxes it is not a free ride.

The TIF funds are used to support the commercial re-development and related public infrastructure that supports the development – to pay for the construction of the public infrastructure over time.

If the TIF continues to generate funds beyond the defined projects infrastructure costs, the revenues remain with the City and can be used for additional TIF eligible infrastructure projects needed to enhance the private development or to maintain the related public infrastructure. This can be a significant amount – see below for estimates.

This is an important tool for both the developer and the City – property owners are sharing in the cost of infrastructure improvements directly benefiting their project while relieving

pressure on the City’s capital and general fund and enable the redevelopment that would not occur without the TIF.

TIF Structure

The TIF setup for this project does not just use the older TIF structure in Ohio (ORC 5709.40) that previous City TIFs use, we are setting up this under newer TIF structures allowed by ORC 5709.41, 5709.42, and 5709.43 (listing these for anyone that would want to look up the law themselves). The newer code allows for more flexibility in how the funds can be assigned and is a better fit for the scale and scope of this project. I am highlighting this for folks who may have had some past experience with TIFs either here or elsewhere. Some of the typical complaints – like with school district payments and rigid allowed projects – are addressed with the newer structure and what we are implementing here.

TIF Estimates

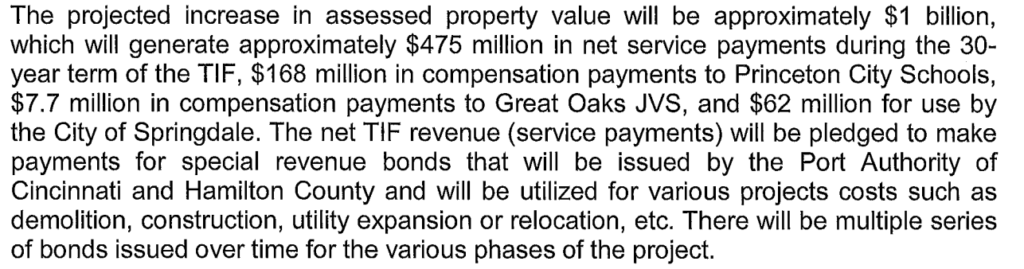

The initial developer estimates of the investments at $800 Million to $1 Billion over 10 years (with half of that coming in Phase One with a planned open date of December 2024) initial projects were released by City Administration. Keep in mind these are initial rough estimates – the project has already changed from the initial estimates upwards of 1.4 Billion in the final. The details of the TIF fund won’t be firmer until outside estimates and valuations come in and as each phase of development firm up.

This is really important – with these estimates, if the development is successful – the compensation agreement with the Princeton School Board would provide $168 Million in payments over the 30 years with payments beginning in 2025 to the district (in arrears for the 2024 completion for Phase 1) with another $7.7 Million to Great Oaks vocational school.

Keep in mind the mall is currently in an older TIF district that with the malls decline the past couple years have generate zero payments to the City (with just over $20,000 budgeted per year currently).

This is truly a situation where the Developer, City, and School Board are partnering to enable this exciting development.

The school also benefits other ways such as the favorable terms and build-out of the proposed STEAM institute at the location. Likewise the City gains residents, a more vibrant core, and favorable terms on a possible updated fitness center at the development.

City TIF Share and Plans

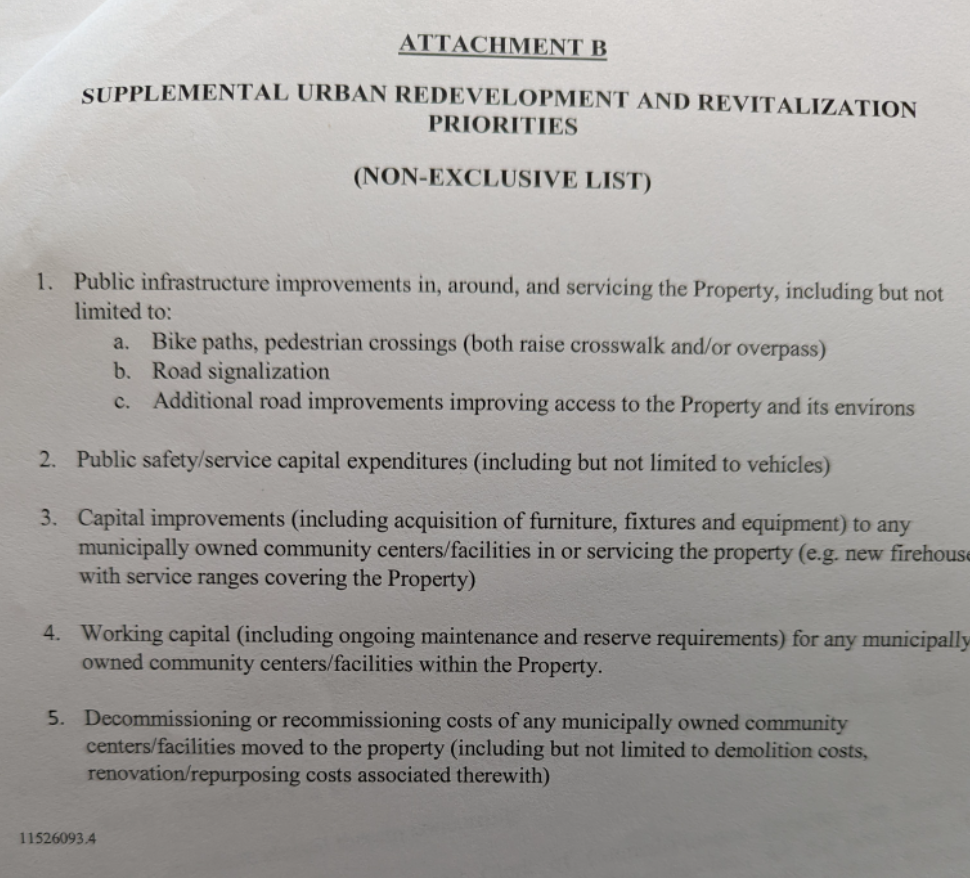

The prior estimates published put the City share of unassigned TIF funds in the ballpark of $62 Million. These funds are allocated after the development bond payments and school payments but oh my – these can be transformation amounts for the City. As part of the passed Ordinance (Ordinance 13-2022) the City outlined what the funds could be used for.

So really the question now is what are the priorities for the City as these funds come in? The funds can not be used for general operating costs – like salaries or consumables (like office supplies or pool chemicals) but capital projects that link back to the development… so many possibilities!

One other important note – related to the previous fitness center relocation discussions – if the fitness center were to move there would be more options for what could be done with the current facility so that will certainly enter into the discussions when the decision to lease at the new location comes before City Council.

What do you think? Let your elected officials know!

email and phone numbers of all your City Council members are online – https://www.springdale.org/city-council/page/meet-your-city-council

and

City Administration as well –

https://www.springdale.org/mayor-clerk-council

or

Connect with your Neighbors –

https://www.facebook.com/groups/333111242219243

Related Links

Note – on July 31, 2023 Springdale released a new website and previous links were not maintained as well as many minutes and agendas offline.

Past Minutes and Agendas: https://www.springdale.org/meetings/recent

Upcoming meetings: https://www.springdale.org/meetings

Request Public Records: https://www.springdale.org/living-springdale/page/public-records-access

Previous Links:

ICRC Meeting Recording Link (4/20)

Written Minutes Link (4/20)

Agenda Link (4/20)